As we approach the end-of-financial-year (EOFY), now is the time to put super arrangements in order, optimise income streams and manage tax. Here are 8 Key EOFY Strategies and Opportunities.

1. Check your caps

If you are considering making a pre-30 June contribution to maximise what you add to super this financial year, it is important first to check the total amount of both your concessional (before-tax) and non-concessional (after-tax) contributions across all your super accounts. Ensure this check includes whether any payments intended for the previous financial year slipped into this financial year too.

The contribution caps for 2024–25 follow:

$30,000 for concessional (before-tax) contributions and

$120,000 for non-concessional (after-tax) contributions.

If your total super balance was $1.9 million or more on 30 June 2024, your non-concessional cap is zero for the 2024–25 financial year. A high balance does not affect your concessional cap.

Your concessional contributions include all your employer’s super guarantee (SG) contributions, salary-sacrifice amounts and any personal contributions for which you plan to claim a tax deduction.

2. Get your contributions in before 30 June

Timing: contributions must be in your super account before 30 June or they will be counted against the next financial year’s limits. Check with your Super Fund the relevant cut-off dates for Direct Debit, BPay and EFT contributions.

3. Consider making a tax-deductible super contribution

You may be eligible to claim a tax deduction for your personal contributions up to the $30,000 (2024/25) concessional contributions cap, but be aware that this cap is for all concessional contributions and includes employer contributions.

Your personal cap may be higher if you have unused cap amounts from the previous five years and are eligible to carry these forward.

Contributions made in this financial year will increase your TSB at 30 June 2025, and this will impact your eligibility to make certain super contributions in 2025/26. For example, if you plan to realise a taxable capital gain next financial year and could benefit from making a larger personal deductible contribution (PDC) under the catch-up rules.

4. Consider making a non-concessional contribution

Non-concessional contributions are contributions you or your spouse make to your super from your after-tax income. They are also referred to as personal or after-tax voluntary contributions.

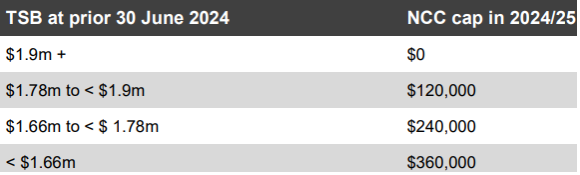

Depending on your total superannuation balance (TSB), if you are aged under 75, you may be able to bring forward up to two years of contributions, giving you a total maximum non-concessional cap of $360,000 for the three years. The thresholds for 2024/25 are:

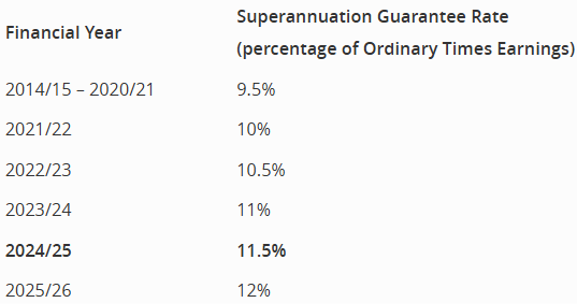

5. Employers: Get ready for a new super guarantee (SG) rate

The SG rate is increasing again in 2025/26 to the government’s target rate of 12%pa as detailed in the table below:

6. Boost your spouse’s super balance

You may be eligible for a tax offset of up to $540 when making super contributions of up to $3,000 into your spouse’s super account, if your spouse’s income is $37,000 pa or less in 2024/25. The offset gradually reduces for incomes above $37,000 pa and completely phases out at $40,000 pa or more. The offset also reduces if the spouse contribution is less than $3,000.

7. Get your salary-sacrifice arrangement ready

You may put in place an agreement with your employer to give up part of your future salary (thereby reducing your taxable income) and investing it into super to boost your retirement savings.

8. Confirm your super income stream payments

An income stream must meet 2 fundamental requirements:

- payment occurs at least annually

- an age-based minimum rate is paid to the member each year (for an account-based pension).

Sources:

Catherine Shepherd B Bus, Dip FP

Paraplanner – Doctors Wealth